Financial Planner vs. Financial Advisor: When it comes to managing money, many people turn to professionals for guidance—but the terms financial planner and financial advisor are often used interchangeably. While both roles involve helping clients achieve financial stability, there are important differences in their qualifications, services, and scope of work.

Regulation and Oversight

Financial planners are regulated by the services they provide. For instance, those who manage investments must register with the U.S. Securities and Exchange Commission (SEC) or state regulators.

What Is a Financial Advisor?

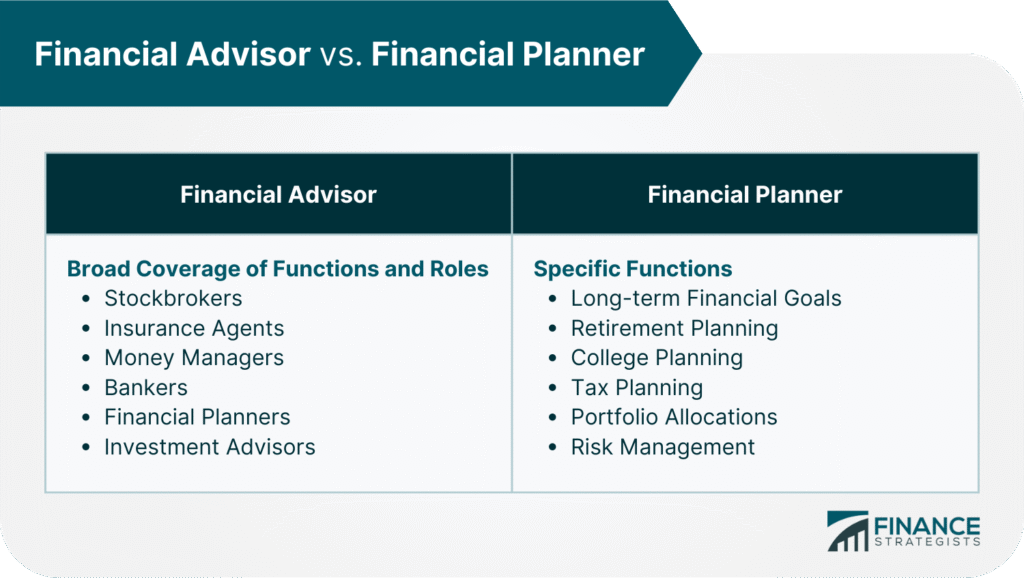

A financial advisor is a broader category of professional who offers guidance in various aspects of personal and institutional finance. Unlike planners, advisors may focus on specific financial products or transactions.

Core Services Offered

Financial advisors can provide:

- Investment management and portfolio allocation

- Securities trading and brokerage services

- Insurance and risk management

- Banking and lending solutions

- Tax planning strategies

- Real estate investment guidance

- General money management

Read about: CRD6 – Article 21c and Its Impact on Third Country Banks and the International Finance Sector

Licensing and Requirements

Unlike “financial planner,” the title financial advisor is subject to stricter licensing requirements. Most advisors must pass the Series 65 exam to work with the public. Additional licenses may be required depending on services:

- Securities licenses for investment advisors

- Insurance licenses for those selling policies

- Federal or state registration for compliance

Financial Planner vs. Financial Advisor: Differences

| Feature | Financial Planner | Financial Advisor |

|---|---|---|

| Focus | Long-term strategies (retirement, education, estate planning) | Broad financial services (investments, insurance, banking, taxes) |

| Credentials | CFP, CFA, ChFC (optional but recommended) | Series 65 required + other licenses depending on role |

| Regulation | Based on services provided (SEC or state) | Heavily regulated by FINRA, SEC, and state authorities |

| Clients | Individuals and families, sometimes small businesses | Individuals, families, institutions, and corporations |

| Compensation | Fee-based or commission | Commission, AUM-based fees, or hybrid models |

Advisor vs. Adviser: Is There a Difference?

Legally, “advisor” and “adviser” are used interchangeably in the financial industry. The SEC often uses “investment adviser,” while firms frequently prefer “financial advisor.” For clients, both mean the same thing, though “adviser” may sound more formal.

Also raed: OPPO F31 Series First Sale: Built for India’s Festive Hustle